When you’re unable to work due to a disabling illness or injury, your long-term disability (LTD) insurance should provide the financial protection you’ve been paying for. Unfortunately, insurance companies don’t always act in good faith. In fact, even when claimants have legitimate disabilities and strong medical evidence, insurers frequently use questionable tactics to deny or terminate benefits. Therefore, understanding the warning signs that your LTD claim may be heading toward an unfair denial can help you take proactive steps to protect your rights under ERISA.

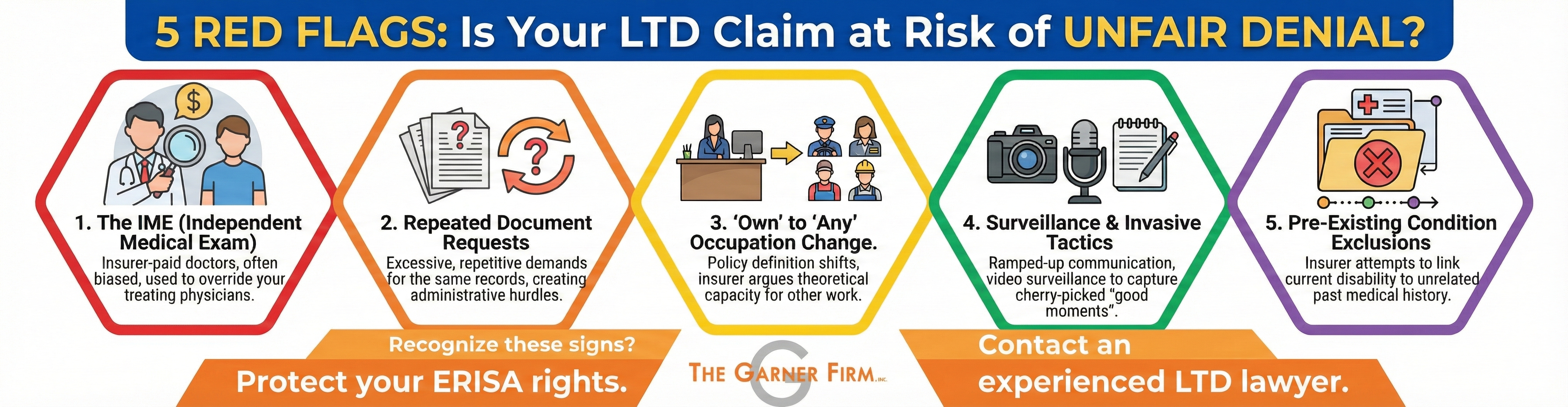

Red Flag #1: The Insurance Company Orders an Independent Medical Examination for Your LTD Claim

One of the most common red flags is when your insurance carrier suddenly requests that you attend an Independent Medical Examination (IME) or subjects your claim to a “peer review” by a physician who has never examined you. Despite the term “independent,” these doctors are typically hired and paid by the insurance company—creating an inherent conflict of interest. Some of them derive a substantial percentage of their annual income from performing insurance company reviews. They know where their bread is buttered.

Moreover, insurance companies often use IME physicians who have a track record of providing opinions that favor claim denials. The examining doctor may spend only 15 to 30 minutes with you. Yet, their brief assessment can be used to override years of treatment records from your own physicians who know your condition intimately. Consequently, when an insurer relies heavily on an IME while dismissing your treating physicians’ opinions, this is a significant warning sign that your long-term disability benefits may be in jeopardy.

Red Flag #2: Repeated Requests for the Same Medical Records and Documentation

Insurance companies have a legitimate right to review your medical records and request documentation supporting your disability claim. However, when your insurer repeatedly asks for the same information you’ve already provided, or makes excessive and burdensome requests for irrelevant documentation, this often signals that they’re building a case to deny your claim rather than fairly evaluating it. (ERISA require insurers to look for reasons to pay your claim, but insurers have a financial conflict of interest that often causes them to look for reasons to deny an LTD claim.)

This tactic serves multiple purposes for the insurance company. First, it creates opportunities for you to miss a deadline or fail to provide a requested document—giving them grounds to deny your claim based on lack of cooperation. Second, the constant barrage of requests can be overwhelming, especially when you’re dealing with a serious medical condition. As a result, if your insurance company seems to be on a fishing expedition, consult with an experienced LTD lawyer who can help you navigate these requests appropriately.

Red Flag #3: Your LTD Claim Approaches the “Own Occupation” to “Any Occupation” Definition Change

Most ERISA long-term disability policies contain a critical provision that changes the definition of disability after a certain period—typically 24 months. During the initial period, you’re considered disabled if you cannot perform your “own occupation.” After this period expires, the definition typically switches to whether you can perform “any occupation” for which you’re reasonably qualified by education, training, or experience.

This transition period is when many legitimate LTD claims are wrongfully terminated. Insurance companies often use this change as an opportunity to argue that while you cannot perform your previous job, you could theoretically perform some other type of work—even if no such jobs actually exist in the labor market or would realistically hire someone with your medical limitations.

Watch for increased scrutiny of your claim as you approach this transition point. Insurance companies may order vocational assessments, increase their requests for documentation, or suddenly question the severity of your condition. If you’re approaching this threshold in your policy, it’s wise to consult with an attorney who understands ERISA litigation before your benefits are terminated.

Red Flag #4: Surveillance, Increased Communication, or Invasive Questioning

If your insurance company suddenly ramps up communication, attempts to schedule multiple phone interviews, asks leading questions about your daily activities, or you notice signs you may be under surveillance, your claim is likely under heightened scrutiny. Insurance companies routinely hire private investigators to conduct video surveillance of LTD claimants, hoping to capture footage that can be taken out of context to suggest you’re not as disabled as you claim.

The problem with surveillance is that it captures isolated moments without context. A claimant with chronic pain might have a “good day” where they’re able to walk to the mailbox or play briefly with their children—but the video won’t show the hours or days of severe pain that follow such activities. Insurance companies will use these cherry-picked moments to argue that you’re capable of full-time work, even when the complete picture tells a very different story.

Red Flag #5: The Insurer Relies Heavily on Pre-Existing Condition Exclusions to Challenge Your LTD Claim

When an insurance company stretches to connect your current disability to an unrelated previous medical condition, this is often a sign they’re grasping at straws to deny your claim. ERISA LTD policies typically contain pre-existing condition exclusions that prevent coverage for disabilities related to conditions you were treated for during a specific period before your coverage began. However, insurers sometimes attempt to apply these exclusions inappropriately, linking your current disabling condition to past health issues that have no genuine connection.

Review your denial letter carefully for any reference to pre-existing conditions. If the insurance company is attempting to link unrelated medical history to your current disability, this is a strong indicator of bad faith. An experienced ERISA attorney can help you challenge these improper denials by demonstrating that your current condition is distinct from any previous health issues.

Understanding Your Rights Under ERISA Section 502(a)

The Employee Retirement Income Security Act of 1974 (ERISA) governs most employer-sponsored long-term disability insurance plans. Under Section 502(a) of ERISA, plan participants have the right to file a lawsuit to recover benefits that have been wrongfully denied. Section 502(a) provides the legal framework that allows you to challenge an unfair denial in federal court.

However, ERISA claims are complex and subject to strict procedural requirements. Before you can file a lawsuit under Section 502(a), you must typically exhaust the insurance company’s internal appeals process. Many claimants make the mistake of handling their ERISA appeals without legal representation, not realizing that the administrative record built during the appeal becomes the evidence the court will review. Federal courts in ERISA cases often do not allow new evidence at trial, which means your appeal is often your only chance to build a complete record supporting your claim.

How The Garner Firm Can Help

At The Garner Firm, we have built our practice on helping employees and insured individuals fight back against insurance companies that wrongfully deny legitimate long-term disability claims. Our founder, Adam H. Garner, has two decades of experience handling ERISA lawsuits in state and federal courts nationwide, including claims for benefits and equitable relief actions under Section 502(a) of ERISA.

Mr. Garner’s background as a former administrator of multi-million and billion-dollar multiemployer benefit plans provides unique insight into how insurance companies and plan administrators make decisions about LTD claims. This insider knowledge allows us to anticipate the tactics insurers will use and build compelling cases that hold them accountable. We have successfully represented clients throughout Pennsylvania, New Jersey, Maryland, and across the country in complex ERISA benefits claims.

Take Action to Protect Your Long-Term Disability Benefits

If you’ve noticed any of these red flags in your LTD claim, don’t wait until your benefits are denied or terminated to seek legal help. The time to act is now—whether you’re facing an upcoming IME, approaching the “any occupation” definition change in your policy, or have already received a denial letter. Early intervention by an experienced LTD lawyer can often prevent a denial or significantly strengthen your position if you need to appeal or litigate your claim.

The Garner Firm represents employees, executives, and professionals throughout Philadelphia, Southeastern Pennsylvania, the Delaware Valley, and Maryland in ERISA long-term disability claims. We also assist referring attorneys whose clients need specialized representation in ERISA benefits litigation. Our firm handles cases on a contingency fee basis in appropriate cases, which means you don’t pay attorney fees unless we recover benefits for you.

Don’t let an insurance company’s bad faith tactics deprive you of the long-term disability benefits you’ve earned. Contact The Garner Firm today at (215) 645-5955 or visit www.garnerltd.com to schedule your free, confidential consultation. Let our experience in ERISA litigation work for you.